Most contractors think they have a solid understanding of job profitability, but owned equipment is a blind spot. It can quietly distort both job costing and billing.

Projects consume resources, and those resources must be captured in job costs. The primary costs to complete a project include:

- Craft labor: captured daily through time entry, with workers able to report what work was performed

- Materials: tracked through delivery tickets and matched with purchase orders

- Subcontractors: recorded periodically based on contract terms and vendor invoices processed through accounts payable

- Rental equipment: recorded periodically based on rental agreements and vendor invoices processed through accounts payable

- Owned equipment: far more difficult to measure, assign to jobs, and cost with precision

So, what makes owned equipment different?

Labor, materials, subcontractors, and rentals usually generate direct, transaction-based costs that are visible and timely. This is because cash must change hands, and someone must get paid.

From an asset costing perspective, owned equipment does generate direct, transaction-based costs:

- Invoices associated with the asset typically get recorded to the fleet number.

- Fixed costs associated with ownership typically have an annual or monthly frequency.

- Variable costs associated with operating often appear in uneven waves — mainly because repairs and component replacement timing is uncertain.

The challenge of job costing owned equipment is spreading known asset costs fairly across the jobs performed. In this blog post, we’ll cover the complexity of tracking owned equipment costs, the risk of not getting it right, and tips on how to track construction job profitability more accurately.

What It Truly Means to Track Construction Job Profitability

Tracking construction job profitability is more than comparing billings to total job costs at the end of the month or quarter. True profitability is measured at the project and cost-code level, where the work is performed and where resources are actually consumed.

Depending on the contract structure, revenue may be recognized through time and materials billings, progress billings, units produced, or other agreed-upon methods. Against that revenue, contractors must account for the direct costs of labor, materials, subcontractors, equipment, mobilization, and transport — along with an appropriate portion of overhead.

For many contractors, the challenge is measuring these transactions accurately and consistently enough to trust the result.

That is why real job profitability depends on both financial data and operational data.

Financial data shows you what was spent and what was billed. Operational data shows where the cost was incurred, what activity drove it, how much work was performed, and which cost code or production unit should carry the burden.

Without that operational layer, even good accounting data can end up attached to the wrong job, the wrong phase of work, or the wrong unit of production. This becomes especially important in construction because the analog processes used to capture field activity are not always reviewed with enough rigor. When field inputs are delayed, incomplete, or estimated, profitability analysis can look precise on paper while still being directionally wrong.

And in this equation, the hardest variable to measure accurately is owned equipment.

Why Owned Equipment Costs Are So Difficult to Track

Owned equipment is difficult to track because it does not behave like most other job costs. Owned equipment is a long-term asset that typically gets consumed over many short-duration projects.

Owned Equipment Doesn’t Generate an Invoice

Rental equipment is relatively easy to see in the financial record. A vendor sends an invoice, and accounts payable processes it. The cost can usually be tied back to a job, period, or contract. Owned equipment does not work that way. Contractors are left to build their own internal method for capturing, assigning, and recovering costs.

That often leads to a patchwork of approaches. Some contractors charge equipment costs to a departmental general ledger and allocate the costs later with a monthly or quarterly basis, or sometimes never.

Some push equipment-related cash costs directly to jobs as they occur, which can feel more like playing hot potato than applying a consistent costing method. Others rely on internal rate sheets, spreadsheets, or static hourly assumptions that may or may not reflect reality.

In many organizations, especially early in equipment management, owned equipment costing is an afterthought rather than a core part of job financial control.

Utilization Is Often Estimated, Not Measured

Even when a contractor has an internal equipment rate, the next challenge is determining how much cost to assign to the job. That depends on utilization, and utilization is often estimated rather than measured with discipline.

A machine may be present on site, but presence is not the same as productive use. Run time, standby time, and engine idle time all tell different stories. A machine that sits on a project underutilized can still carry meaningful ownership and operating costs.

If run time, standby time, and idle time are not distinguished, the wrong cost basis gets extended to the wrong work.

When hours are assigned to the wrong cost code, even good financial data can be extended across the wrong operational units. The result is a job-cost picture that looks precise on paper but is directionally wrong in practice.

Depreciation, Maintenance, Fuel, and Transport Are Disconnected

Another reason owned equipment is so difficult to track is that the full cost picture is fragmented across multiple systems and teams.

- Many owning costs, such as depreciation, property tax, insurance premiums, and financing costs, live in the accounting system.

- Fuel may live within fleet card data, tank logs, or feedback from fuel and lube teams.

- Maintenance and repair history often lives in the shop’s computerized machine maintenance system.

- Telematics data lives on a separate platform.

- Transport and mobilization may be tracked operationally but not consistently reflected in job cost.

None of these sources automatically translate themselves into accurate job costing, and the fragmentation creates administrative burden and analytical blind spots.

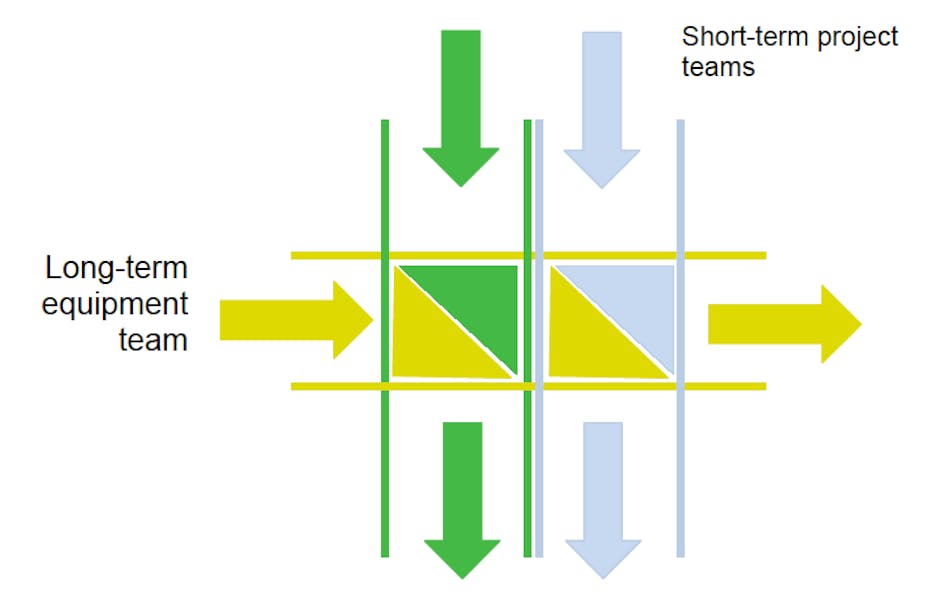

This is where the distinction between short-term project management and long-term equipment stewardship becomes important.

- Project teams care that equipment shows up, performs, and supports production at the lowest apparent cost on their job.

- Equipment teams, by contrast, are responsible for the full lifecycle of the assets across many jobs, over many years.

Those are both valid perspectives, but they do not naturally reconcile themselves inside most job cost systems.

Equipment Costs Occur in Spurts, Not in a Smooth Pattern

Equipment cost does not occur in a neat, uniform rhythm. A machine may work productively for days, weeks, or months while generating very little repair expense, then suddenly require a major service, component replacement, or failure-related repair.

There is also often a lag between cause and effect. A machine failure that appears today may have been set in motion months earlier by poor fuel quality, improper operation, missed service, or harsh site conditions. By the time the cost arrives, the original job, operator, or decision that contributed to the issue may no longer be obvious.

In other words, the machine may “earn” steadily while the spending shows up later — in uneven bursts. That disconnect makes owned equipment fundamentally harder to job cost than the other cost categories discussed earlier.

The Risk of Not Accurately Tracking Equipment Costs

Put simply, if owned equipment is not tracked accurately, the business does not just lose precision; it starts to lose trust in the numbers and between departments.

When that trust breaks down, profitability, billing, and fleet strategy all become harder to manage. Poor equipment costing does not just distort the numbers; it can also erode trust across teams that rely on the same version of the truth.

Inflated Project Margins on Paper

Equipment-heavy projects can appear healthier than they really are simply because the true cost of ownership, operation, idle time, fuel, transport, and maintenance never fully makes it onto the job.

If equipment hours are estimated, averaged, or assigned too late, the job may not absorb the full burden of the assets it consumed. Some projects become “false winners,” not because they performed better, but because they were never charged for the true wear, fuel, downtime, and ownership burden of the fleet used to complete the work. The result is distorted margins, unreliable forecasting, and false confidence in project performance.

Interdepartmental Tension

When equipment costs are not grounded in clear operational data, friction can develop between equipment managers and construction operations. Operations teams may feel they are being charged for cost they cannot verify, while equipment managers may feel the field is consuming fleet resources without fully accounting for the burden placed on the asset.

Instead of working from a shared source of truth, both groups can end up debating hours, usage, standby time, transport, or who should absorb the cost. That kind of mistrust slows decisions, weakens accountability, and makes cross-functional planning much harder.

Underbidding Future Work

When leadership relies on distorted historical job cost data, estimators are forced to build tomorrow’s bids on yesterday’s incomplete assumptions. The result is a repeated cycle where the company continues to price work too aggressively, not because field execution failed but because equipment cost was never fully understood in the first place.

Accurate allocation matters because it directly improves reporting accuracy, estimating assumptions, and future bid predictability.

Third Party Billing and Dispute Risk

When equipment activity is not tied to trustworthy operational data, internal cost allocation becomes harder to defend, and external billing becomes more vulnerable to dispute. Underreported hours, wrong cost codes, stale field data, and delayed entry into the ERP all create leakage. Invoices go out late, customers question the charges, and internal teams end up debating who should absorb the cost.

Leadership Level Risk

At the leadership level, the biggest risk is reduced financial visibility.

CFOs and operations leaders need to know not just where equipment is, but whether it is recovering costs, supporting margin, and being deployed effectively.

When equipment data remains disconnected from job financials, executives are left making decisions from reconciled estimates weeks after the fact rather than from timely, decision-grade information.

As a result, the poor data weakens WIP visibility, clouds cost-to-complete and makes it harder to act before a margin problem becomes a financial result.

How to Track Construction Job Profitability More Accurately

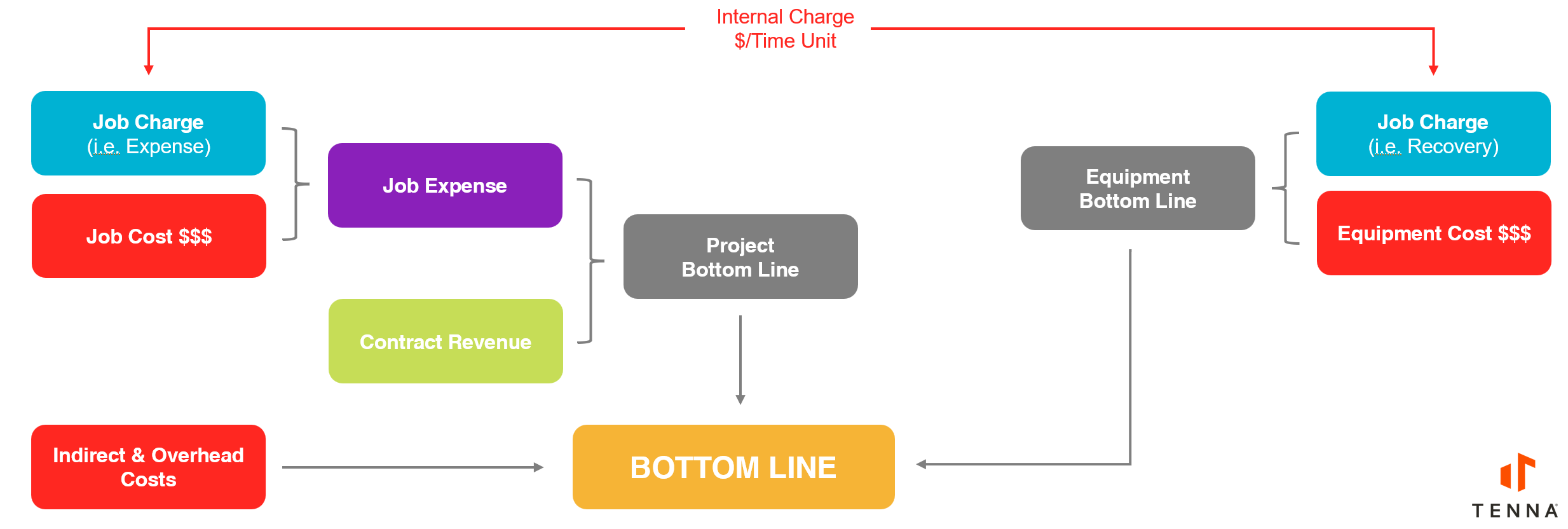

The image below provides a simple framework for separating and identifying the cost categories that impact the business. The red blocks represent hard dollars going out.

- Job Cost = craft labor, subcontractors, materials, and rental equipment

- Equipment Cost = mechanic labor, parts, rent/purchase, insurance

The blue blocks represent interdepartmental charge for owned equipment where hard dollars aren’t exchanged. The key is defining the appropriate rate type and the cost per unit of time:

- A run-time rate would typically include both owning and operating costs.

- A standby-time rate would typically include owning costs only.

- Other rate structures may include hourly, daily, weekly, or monthly charges

There are many options depending on how the contractor wants to recover cost. The key takeaway is: rates are only as good as the cost basis and utilization assumptions used to develop them.

→ For more information regarding best practices and establishing rates, see Mike Vorster’s Equipment Economics V2

Step 1: Define Your True Cost of Ownership

To manage a system like this effectively, contractors must first understand their true cost of ownership. That may come from their own internal cost history, or from a reliable benchmark such as Blue Book rates that align with their work profile, market, and region.

Without a defensible cost basis, even the best utilization data will lead to questionable results.

Step 2: Capture True Equipment Utilization

Once cost is defined, the next step is capturing the time units that reflect actual equipment consumption. These operational inputs are what drive accurate cost allocation. If utilization is estimated rather than measured, the resulting job cost will always be less reliable.

The goal is to distinguish between meaningful categories of activity, such as run time, standby time, idle time, and underutilization, so the burden placed on the asset can be assigned more accurately.

Telematics-driven workflows matter because they replace assumptions with timestamped activity records that support both job costing and billing accuracy.

Step 3: Allocate Equipment Costs to Jobs Automatically

Telematics can provide a robust set of data points related to engine state, location, and movement. When paired with geofences for projects, sub-projects, change orders, or scopes of work, this data can help determine where equipment was operating and how it was being used. That significantly reduces the burden on field personnel and improves the consistency of cost allocation.

Step 4: Tie Equipment Costs to Revenue and Billing

When contractors have a complete view of asset location, activity, and job cost, it becomes much easier to manage billing and margin performance. Better equipment costing supports more accurate billing, clearer internal cost recovery, and a stronger understanding of true project profitability.

It isn’t that contractors do not want this visibility. The problem is that, until recently, there has not been a simple way to unify it.

Read more about tying equipment costs to project financial performance.

The Industry Gap: Telematics and Financial Systems Still Operate in Silos

The industry gap isn’t caused by lack of software or data. The data needed lives in separate systems that weren’t optimized for the contractor’s workflow.

- Telematics providers are excellent at tracking equipment location, engine activity, utilization, and machine health.

- ERP systems are designed to manage accounting, accounts payable, payroll, and financial reporting.

- Fleet and maintenance systems help shops manage inspections, repairs, preventive maintenance, and parts.

Each system serves an important purpose, but each one only captures part of the picture.

What is still missing is a practical way to connect owned asset utilization directly to job-level financial performance.

That gap matters because owned equipment does not enter job cost through a clean vendor invoice. It has to be interpreted, assigned, and extended through a cost model that reflects how the asset was actually used.

Today, most contractors are still forced to bridge that gap manually, relying on spreadsheets, delayed allocations, rate tables, and fragmented records from multiple departments.

The result is a market-wide disconnect. Contractors can often see where equipment was, how long it ran, and what it cost the business in total, but they still struggle to connect that information directly to real-time job profitability.

There is currently no easy, contractor-friendly way to connect owned equipment costs directly to real-time job profitability. That is the gap the industry still needs to close.

A New Approach to Connecting Asset Data with Job Financials

The next step forward is a model that connects equipment activity directly to job financials.

In that model:

- Equipment usage automatically translates into job-level cost allocation.

- Owned asset depreciation and operating burden become visible at the project level and scope of work.

- True cost of ownership flows directly into job cost reporting, instead of being buried in departmental accounts or reconciled weeks later.

- The result is greater visibility for project managers, equipment leaders, and finance teams, all of whom can better understand the margin impact of equipment activity in near real time.

Stay tuned as Tenna introduces Asset Financials — a new way to track equipment costs and transform how contractors measure job profitability.

Conclusion: The Future of How to Track Construction Job Profitability

Tracking construction job profitability without owned equipment costs gives contractors an incomplete picture of financial performance. To measure profitability more accurately, contractors need more than basic job cost reporting.

Contractors need:

- real utilization data

- visibility into true cost of owning and operating

- seamless cost allocation

- reporting that is credible enough for both operations and finance

When those pieces come together, owned equipment transforms from a blind spot into a connected financial picture that helps contractors:

- price work more accurately

- recover cost more consistently

- improve trust between departments

- make better decisions about fleet strategy

The contractors who win in tomorrow’s market will not just track their equipment. They will connect it directly to job financial performance.